Banks are seen as close to the end of the rate-increasing cycle, with hope that inflation has topped out.

Central Banks Have Yet To Script Final Act Of Inflation Fight As Risks Rise

Banks are seen as close to the end of the rate-increasing cycle, with hope that inflation has topped out.

Major central banks may be deep into their drive to raise interest rates in hopes of killing inflation, but the endgame remains far from clear as price increases prove harder to slow than expected, and analysts caution that financial markets could still break along the way.

The U.S. Federal Reserve, the European Central Bank and the Bank of England are all still raising rates, and policymakers are open about the massive uncertainty surrounding their projections and the risk they may have to do more than expected.

But all are also felt to be closing in on a peak interest rate for this round of monetary policy tightening while holding fast to projections that inflation will slow steadily over the next year or two without a major blow to economic activity.

That view has received a sceptical response from top global policymakers and analysts who see a world where persistent shortages of labour, cleavages in global supply, and wobbly financial markets may force a choice between higher and longer-lasting inflation, or a deep recession to fix it.

In the more fragmented global economy emerging from the COVID-19 pandemic, "we are going to be hit by more supply shocks, and monetary policy faces much more serious trade-offs," International Monetary Fund First Deputy Managing Director Gita Gopinath said in a forum during the IMF and World Bank spring meetings in Washington last week.

Her comments were echoed by others who feel the narrative shared by three top central banks of relatively cost-free disinflation rests on shaky ground.

It is certainly out of step with the past. Gopinath noted there was "no historical precedent" for high inflation to be squelched without rising unemployment.

SLOWDOWN OR RECESSION?

The argument that this time will be different, moreover, rests on a shared hope that inflation in the post-pandemic world will behave much as it did before - tepidly, in other words, anchored lower rather than higher, and with little need for subpar output or rising joblessness to control it.

It's a view that, while skirting the word, still regards the current bout of inflation as at least somewhat transitory, the product of ongoing readjustment to the once-in-a-century shock of the pandemic and the added pressure on commodity prices from Russia's invasion of Ukraine.

Interest rates are being raised to check demand enough to ease price pressures and keep public inflation expectations under control as those distortions pass and previous inflation trends resurface.

Notably, after one of the most violent blows to the global economy, intensifying geopolitical tensions and a still-unresolved war in Europe, Fed policymakers' median estimate of a long-run policy rate consistent with stable inflation remains at 2.5% - the same as it has been since June of 2019, a moment of peak faith in the notion of a largely deflationary world.

The prospect of inflation falling alongside a gradual return to the pre-pandemic state of affairs is implicit in how central banks are framing the path forward.

Among the Fed, ECB and BoE, only the British central bank projects a recession will be needed to slow inflation - only a mild one at that. The ECB expects to win its inflation battle with no change in the unemployment rate. U.S. central bank officials have split the difference, projecting a modest one-percentage-point rise in the unemployment rate this year from its near-historic low of 3.5%, and slow, but continued, economic growth.

Against that outlook, Fed policymakers last month indicated that one more quarter-percentage-point rate increase at their May 2-3 meeting, which would raise the policy rate to the 5.00%-5.25% range, could be the last of this tightening cycle.

The BoE and ECB are likely further from rate-hike pauses, but a Fed halt would send a powerful signal that the era of synchronized tightening is over, with central bankers entering a holding pattern to wait for the impact of tighter financial conditions and normalizing economies to be felt on prices.

'UNTIL THE LABOR MARKET QUITS'

That is where the data and the narrative part ways.

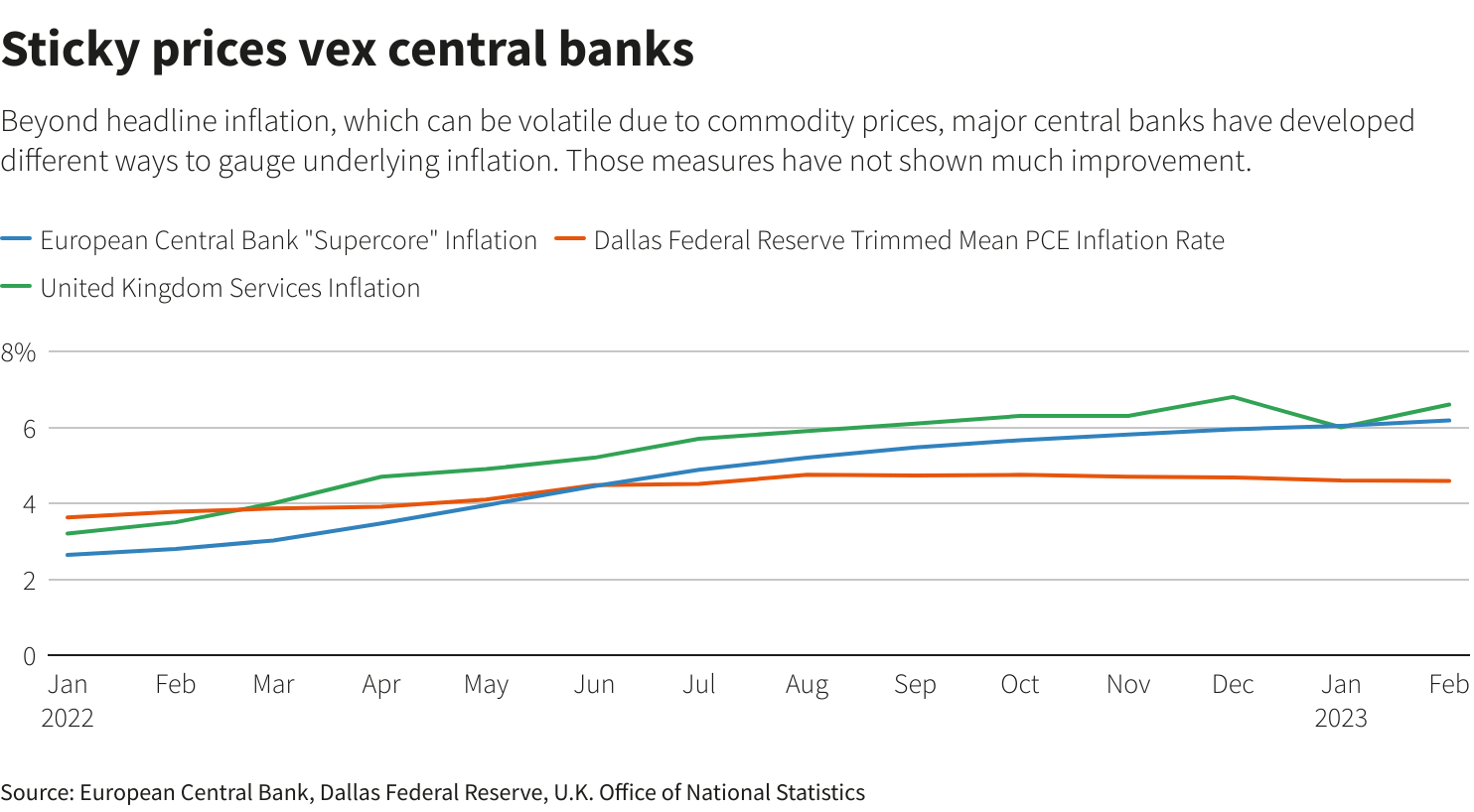

There have been some notable declines in inflation across Europe and the U.S. Yet they have been driven by the most volatile components - particularly energy costs - while underlying inflation, especially in the most labour-intensive industries, has been slower to move.

While the core ECB expectation is for falling profits, improving supply chains and lower energy prices to bring down inflation, some officials worry that, in a world of labour scarcity, that won't be enough.

"It is not a given that we will return to price stability over the medium term," even after the fastest rate hikes on record, Bundesbank President Joachim Nagel warned last week during a speech at the Peterson Institute for International Economics in Washington.

Martins Kazaks, Latvia's central bank chief, said the risk of a recession was still "non-trivial," with a host of factors still putting pressure on prices.

"Corporate profit margins still remain high, wage pressures are strong and the labor market is tight," Kazaks told Reuters. "All these point to the view that inflation persistence is relatively strong and that rates still need to go up."

For the Fed, different policymakers offer different ideas about the forces that will lower inflation as high interest rates slowly cool demand.

Fed staff and a growing number of market participants and economists, however, don't see it working out absent a recession - something that Jason Furman, a Harvard University professor who was the top White House economic adviser in the Obama administration from 2013 to 2017, feels is implicit in policymakers' projections even if they avoid the word.

The U.S. unemployment rate has never risen one percentage point over nine months without a recession, and the 0.4% growth in gross domestic product projected for 2023 would, after a strong first quarter, mean output would shrink for the rest of the year.

"I think they do have a coherent story, which is that they're going to cause a recession," Furman told Reuters on the side-lines of the IMF and World Bank meetings. "You don't hear it very clearly ... I think they also have a hope for a 'soft landing,' and that probably shows up in being a little bit more timid in their policy" than might ultimately prove necessary.

Furman was referring to a scenario in which monetary tightening slows the economy, and inflation, without triggering a recession.

If the steps expected so far have avoided a major shock to jobs or financial markets, it's the steps potentially required after that where things get riskier.

The Fed "is not going to quit until the labor market quits," said Randall Kroszner, a former Fed governor who is now a professor at the University of Chicago's Booth School of Business. With interest rates now moving above the rate of inflation in the U.S. and becoming ever more restrictive, "that is where the rubber is going to hit the road ... I think it is going to be very hard to avoid something moving down and moving down relatively quickly."

(Writing by Howard Schneider; Editing by Dan Burns and Paul Simao)

Central Banks Have Yet To Script Final Act Of Inflation Fight As Risks Rise

Thanks for signing up to Minutehack alerts.

Brilliant editorials heading your way soon.

Okay, Thanks!