Sands shift fast and far online. In this long-read Lori Goldberg looks at the big changing themes that all digital marketers must understand.

The term “Paradigm Shift” is overused particularly in high-growth sectors such as advertising and digital marketing, where paradigms are constantly shifting but not uncharacteristically so.

It’s vital to separate evolving strategies from true paradigm shifts; evolving strategies are like ripples in an ocean that are quickly absorbed by the paradigm, whereas shifts are tidal waves that create massive changes requiring adaptation by the marketplace. Adaptive marketers – being opportunistic – crave the shifts for the opportunities they bring.

A “paradigm shift” is a profound change in a fundamental model that leads to new problems and the pursuit of new solutions. The term was coined by American psychologist and sociologist Thomas Khun (1922 – 1996). Shifting paradigms are not easy to agree on, however. Khun speculated that two people might often view paradigms very differently, often seeing “different things when looking at the same sorts of objects.”

Case in point:

The image below is a common example of how we may disagree on shifting paradigms. Is it a duck or a rabbit?

But if we see things differently, one person’s problem could be another’s solution. Adam Briggle of Science Progress wrote, “Who gets to write the rules – those who see ducks or those who see rabbits? Each group uses its own paradigm to argue in that paradigm’s defense.”

Armed with this understanding of paradigm shifts, this series will examine 5 areas within digital marketing where shifts are occurring and offer prescriptive advice on how adaptive marketers can take advantage of new opportunities.

Part One. The mobile-first approach

Part Two. The fall of the banner ad

Part Three. The Google & Facebook duopoly

Part Four. Technology-driven bulk media buying

Part Five. Ad quality in question

Part One: Advertisers Adopt a “mobile-first” approach

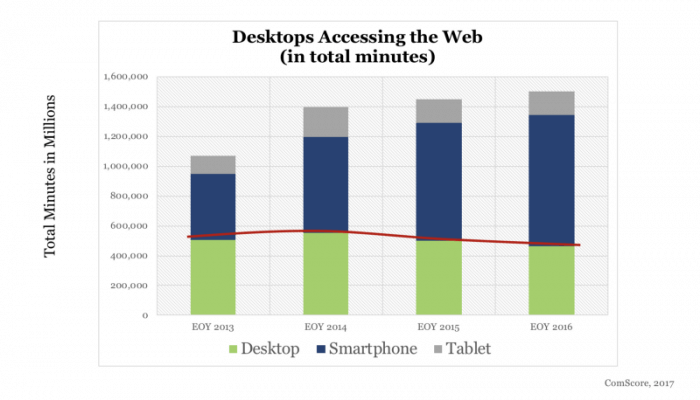

Today’s smartphones are replacing the desktop and laptop computer with equally powerful processors, web-access, and speed that afford user freedom and spontaneity. There was a consensus years ago that a “mobile advertising strategy” was needed by advertisers given what we knew of the mounting smartphone adoption and shifts to mobile browsing, responsive websites, and mobile wallet capabilities.

Today, we have evolved - or perhaps shifted - to a mobile-first strategy. Statistics show for the first time that mobile phones are out-pacing desktops in accessing the web. As a result, the Internet Advertising Bureau announced at the end of 2016 that, “Mobile ad revenues account for more than half (51 percent) of all digital ad revenues for the first time.” Mobile-specific content and apps including Instagram, WhatsApp and Snapchat untether users from their desktop.

What’s more, mobile devices are being used to complete with brick and mortar stores at the point of purchase. For example, consumers seeking the latest hiking shoes are able to experience the product in a local store, then spontaneously purchase online from a low-priced competitor during their in-store visit.

Desktops will not fade quietly. Their relevance remains high with increased Web usage in streaming video and for making large web-based transactions. Consumers find desktops more user-friendly here for research-heavy purchases such as a new mattress, automobile, and home. However, research for these larger items may also occur on mobile before shifting to the desktop as a more trusted device for purchases.

Implications and opportunities for adaptive marketers

A paradigm shift to “mobile-first” is occurring particularly as a result of mobile maturity - It’s more than a phone but a gateway to content, purchasing capabilities, and transactions. The entire web is being re-coded to fit the phone with responsive design. Given this paradigm shift, consider the following opportunities for adaptive marketers:

· Don’t stop at simply being responsive. Marketers need to push forward with mobile-first campaigns, content and design.

· Prioritize the mobile experience for users and where applicable, drive them back to their desktop if larger transactions are a goal.

· Optimize page speed to load quicker, benefiting mobile users

· Understand consumer sentiment and adjust search terms for consumers that may be wanting to try a product at a competing local store, then buy from your website for a lower price.

· Google is penalising non-responsive sites by down-grading their rank in search results by a small margin. If you’re not mobile-ready, your search rankings may be suffering.

8 in 10 of consumers would stop engaging with content that doesn’t display well on their device – Adobe.

In summary, user data and advertiser spend indicates a paradigm shift away from desktop computers. Smartphones are no longer a secondary option in terms of technology, capabilities and speed. In fact, the mobile user delights in the spontaneity of Instagram, Snapchat, WhatsApp and more.

While desktop has seen gains in video consumption and trust in as a transaction tool for large purchases, advertisers are wise to think mobile first in designing campaigns, technical responsiveness, speed, and the sentiment of point-of-purchase online shoppers seeking competitive prices.

Part Two: The fall of the banner ad

Banner ads, or display, have been the bread and butter of ad publishers for a long time. Today, they tend to clutter the web as a tool for branding, not clicks nor conversion. They have fallen in price, becoming easier to buy, and inventory is plentiful as the ever-expanding web keeps finding new ad real estate for banners to populate.

In part two of Paradigms at War, we look at the plight of the banner ad and ponder its future as advertisers respond to a paradigm shift that demands a reduction in ad clutter, improved performance, and mobile friendly viewability.

Previously, banner ads were an ideal format for desktop web browsers. Their variety of shapes and sizes were tailored to advertisers wanting high visibility, branded design, and of course - clicks.

Today, with advanced ad tracking and analytics, we know that up to 50% of banners ads are never viewed by the consumers (comScore 2016), introducing us to the term “Viewability”. Advertising standards have rushed to redefine what a viewable ad is while advertisers fume over the lack of transparency.

Digital advertising, like radio, TV and print is somewhat based on the ads “opportunity to be seen” by consumers. Just as a radio listener may turn down the volume during an ad or a television viewer may run to the kitchen during a Superbowl commercial, there is no truly scientific way to count each individual’s presence and attentiveness for the duration of an ad.

Advertisers are buying the ads’ opportunity to be seen or heard by an estimated audience. Impressions are similar. Some ads may appear below the fold - near the bottom of the Web page - and never seen by the consumer, much less be properly digested, read or understood. Previously, impressions indicated that the ad loaded into the page – nothing more.

IAB considers an ad viewable on a desktop computer if 50% of the ads’ pixels are in view for a minimum of 1 second. For video, 50% is required for 2 seconds. For larger display ad units 30% is required for at least 1 second.

But with lack of enforcement, defining an ad as viewable is just that: a definition. We have yet to enter the age of enforcement.

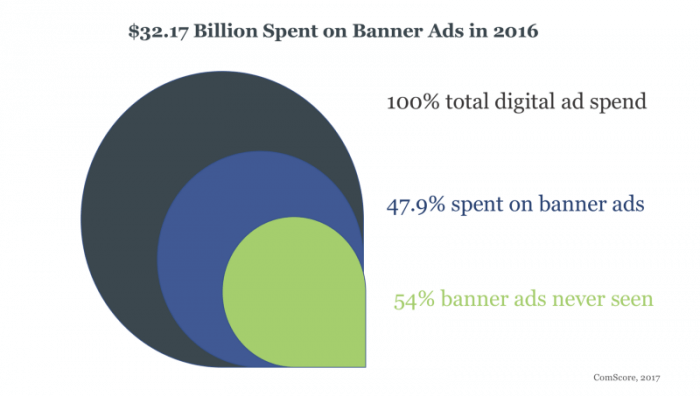

Banner ads account for 47.9% of all digital advertising spending in the United States, and are projected to reach surpass $33 billion by end of 2017. At the same time, however, as much as 54% of all display ads are never seen, and at least $7 billion is spent serving ads to nonhuman "bots.” (comScore, 2017)

As a result, browsers such as Firefox were among the early creators of ad blocking tools which offer users a respite from the popping and pulsating banner ads that clutter pages, slow browsers, and create an otherwise poor user experience. Today, every browser, including Chrome, has a popup blocker.

In many cases they are turned on by default once the browser is installed. As a result, the price of banner ads has dropped along with their value to advertisers. Despite this, inventory of ads remains high, spending on banners ads continues to increase and real estate to host these ads is expanding, even into the dark edges of the Web where tremendous fraud can occur.

$32.17 Billion Spent on Banner Ads in 2016

Technology such as trading desks and programmatic markets make buying and selling banner ads easier than ever, further driving prices down but layering in better targeting capabilities to maintain value. Viewability is not just a concern for digital advertising. It happens across all forms of digital and traditional/print, television and radio media. Regardless, spend continues to rise and the banner market remains hot.

Implications and opportunities for adaptive marketers

A paradigm shift in banner advertising is occurring as consumers are becoming so overwhelmed by banner ads that the valuable consumer experience is suffering. This is a fundamental threat to consumers reacting to those ads. Browsers backed by Mozilla and Google are responding to defend the consumer experience. In turn, consumers are wanting original compelling content instead of blatant ads.

Native advertising, content marketing, and video storytelling have shown to hold consumers attention longer and convey entertainment and information in the form of an ad. This is a trade that consumers are willing to make: ‘advertise to me, but entertain and inform me at the same time.’ The traditional paradigm including ads and consumer response if shifting towards premium content that tells a story. Given this paradigm shift, consider the following opportunities for adaptive marketers:

· Consumers want original compelling content - everywhere

· Native advertising satisfies viewers; focus on quality of information in exchange for lasting attention; Video and storytelling attracts and holds viewers longer than traditional ads and banners

· Reduce frequency and clutter. Failure to do so may frustrate consumers and cast your brand in a negative light

· Promote better ad behaviors:

o Prevent audio and video ads from auto-playing

o Don’t slow browser performance with ad-lag; keep load times fast

o Provide seamless one-click to desired result

In summary, consumers are wanting quality ads over vague and plentiful. Ad-lag and intrusive ad behaviors that slow browser performance create a negative user experience and erode consumer trust. Browsers backed by Google and Mozilla are responding to block ads and protect consumers, ultimately wasting money spent and rendering 50% of banners and not viewable (but paid for).

The occurring shift has visual storytellers including Instagram and Snapchat engaging with consumers for longer periods of time and in more compelling ways. Native advertising is welcomed by consumers willing to exchange their time and attention in exchange for valuable information.

Part Three. The Google & Facebook duopoly

What sets advertising publishers apart is their ability to target ads at specific consumers and earn a measurable result, then adjust, retarget and advertise again. Google, with its algorithmic ability to translate consumer sentiment, context, and intent into the right ad, right time, right place skyrocketed the search giant into the advertising space, claiming market share from television, print and radio in the early days of the new millennium.

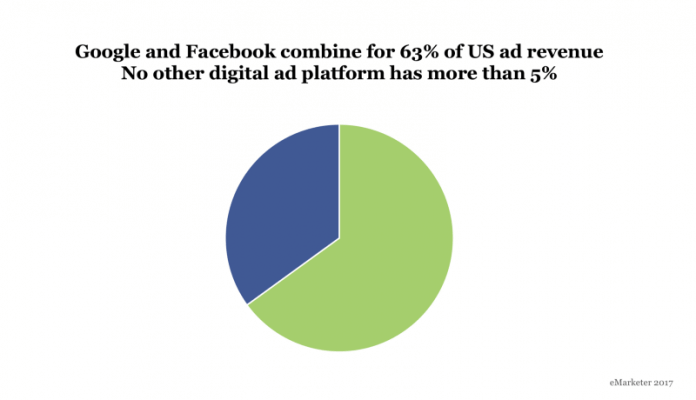

Facebook later took advertising intel to a new level with ad targeting based directly on consumers likes and dislikes within their user profile. This has all evolved significantly as you know and today the two are positioned and a duopoly in digital media, with no single competitor owning more than 5% of the digital ad market. Like any paradigm shift, this duopoly can be viewed in many ways with many benefactors and detractors.

With any duopoly comes a fear the service will erode and prices rise, leading to a stickier product for advertisers with few competitive options. In Spring of 2017, General Motors, Walmart, Verizon, AT&T and Johnson & Johnson cut spending on Google and YouTube when a lone journalist makes it public that their ads were appearing alongside neo-Nazi groups, videos promoting terrorism, fake news and the like.

In March 2017, AdAge wrote, “The resulting press coverage has sparked a full-fledged advertiser revolt.” The issue of “brand safety” is now a real thing. Brands are wanting greater transparency into the content adjacent to their ads. In July, YouTube issued new brand safety rules and removed ads from some offensive content.

Matt Brittin, Google’s president of business and operations in Europe, the Middle East and Africa, reportedly apologized for the brand safety issues affecting advertisers and acknowledged that the problem is a global issue.

The underlying sentiment is this: When Google alone dominates search, what are its obligations for full transparency? Competition can play a key role in ensuring that deeper awareness and transparency tools are provided to make advertisers aware of where their ads are appearing. In the case of Brand Safety, it was discovered by a journalist who saw the ads and took screenshots, not by any means germane to the ad network.

Recently, Verizon has taken on the task of being the transparent ad network, vowing to protect brand safety within its “Oath” network, which includes Verizon properties AOL, Yahoo!, Tumblr, MSN, Huffington Post, Flickr, BrightRoll and more. Alternate networks and rising stars include Snapchat are offering quality video and storytelling popular with users. Oracle (who recently acquired YouTube competitor TubeMogul), MediaMath, Rubicon Project and Adobe are all committed to providing alternatives, as is Amazon who is developing an ad supported video streaming channel.

Implications and opportunities for adaptive marketers

With any paradigm shift comes new problems and new opportunities, and this is no different. Verizon’s Oath is taking advantage of what they perceive to be a weakness on Google’s part: brand safety. Slowly, a third ad network may be forming. But unlike many paradigm shifts, this one still favors Google-Facebook in many ways.

They are massively successful brands and offer new and better options for advertisers every day. This is not a case where the duopoly is failing to remain competitive. While not perfect, as indicated by the advertiser revolt, they are vastly sophisticated ad networks with leading edge services, features and support. Given this paradigm shift, consider the following opportunities for adaptive marketers:

· With competition, advertisers get the features and transparency they need

· Consider independents Rubicon Project, Adobe, MediaMath, Amazon; Snapchat stories hold audience well

· Verizon’s Oath collective vows brand safety to attract advertisers

· Amazon working on ad-supported Prime video

In summary, the paradigm shift to the Google-Facebook duopoly is nothing new in the realm of digital marketing. However, the stakes are much higher today than in the early days when Google and Yahoo! were dominant.

With few ad publishing choices, companies may look for work directly with these publishers instead of utilizing third parties and agencies to manage the relationships, however schooling themselves on media buying and management may be unlikely given bandwidth to manage not only creative but media, too.

The opportunity inherent in any monopoly (or duopoly) is for new brands to enter the space that can fill the perceived weaknesses in the market and there are plenty examples here.

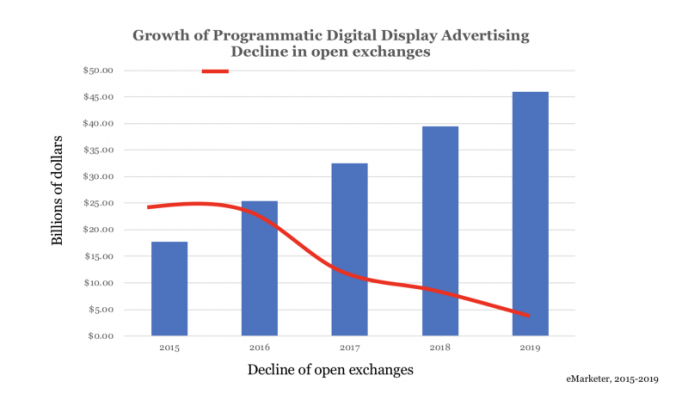

Part Four. Technology-driven bulk media buying

The market has exploded with advertising opportunity and artificial intelligence-based technologies, including programmatic and trading desks, that have allowed media strategists to tame the marketplace. However, greater efficiency coupled with expanding inventory and demand has proved to be a double-edged sword.

The technology also stands accused of lowering ad quality, creating opportunity for fraud, and increased margins by third-party managers. Despite this, the value of this artificial intelligence-driven technology is growing while banner ad prices are falling.

Previously, programmatic became a popular artificial intelligence for efficiently selling remnant ads on public exchanges. Programmatic exchanges soon offered more than just remnants, even selling offline traditional ads.

Demand for ads continues to grow and inventory of ads increases thanks to the ever-expanding Internet that never fails to find more Website pages to advertise on – including some nefarious locations such as click farms. The banner ad basically became traded as a commodity – cheap and plentiful. Ad prices remain healthy given the value-added benefits of superior ability to track performance.

While the tech remains strong, the paradigm shift is occurring in the exchanges. Ad buyers are using programmatic technology to buy from public ad exchanges and private ad exchanges, each offering worthwhile benefits. Public exchanges include publishers such as Google, Yahoo, and OpenX offering low cost and lower-quality ads.

These public exchanges are believed to be sources of fraud, ranging from click farms to bots trolling the Web, responsible for grabbing over $7 billion in click payments. This is not to say all public exchanges are bad. Advertisers need to calculate the ROI they want from any campaign and determine if they are getting the desired results. Google, for example sells low cost ads on public exchanges but also uses ad blockers in its Chrome browser to block similar ads.

Private exchanges – recently including 100% of The New York Times’ ads – offer higher quality exchanges run by major publishers. Ads are carefully selected using trading desks or demand-side platforms providing greater transparency and higher prices.

The paradigm shift here is less about changes in technology and more about how and where that technology is used. The use of programmatic in public exchanges is falling rapidly. Brands are taking programmatic in-house to shave margins and offer what they feel is better quality control.

Likewise, agencies are utilizing black listing to effectively remove poor quality publishers and targeting white lists of pre-approved publishers such as Yahoo!, New York Times, and Buzzfeed for the assurances they bring. In some cases, agencies cultivate their own white lists or use public ones.

However, use of programmatic is climbing rapidly in private exchanges, perhaps as a response to viewability and fraud issues. Meanwhile Google, Facebook, Instagram and Snapchat are pushing for better quality ads driven by native storytelling, video and stickier concepts that hold and retain viewers. Snapchat will soon be making it’s “Stories” concept available outside the app for greater distribution and will certainly invite more competition.

Implications and opportunities for adaptive marketers

The opportunities within technology-driven bulk media buying are to focus on the contributions of artificial intelligence that lead us to making smarter and more efficient buying decisions. The rise of programmatic will forever be linked with poor ad quality and clutter the it amplified, however that’s a bit unfair. An analogy would be that powerful engines led to more speeding tickets. True, but that’s not the point of the technology.

The paradigm shift will continue making ad buying smarter and the collateral damage here is that poor quality ads will benefit, too. IBM is now using weather to predict consumer mood; Amazon’s Echo is becoming a voice-activated search engine. Leaders in artificial intelligence and private exchanges have the most to gain as a result. Given this paradigm shift, consider the following opportunities for adaptive marketers:

· For ad buyers and sellers, the desire and need for greater control is moving them toward more private exchanges

· Re-define programmatic as a mechanism for efficient ad buying, not exacerbating poor ad quality

· Defend your programmatic buys: focus on analytics and transparency

· Engage on public exchanges with goals in mind; focus on your ROI and benefit from the cost savings

· Look for new opportunities where programmatic is further enhanced by artificial intelligence

In summary, the shifting paradigm here is about artificial intelligence influencing bulk advertising technology for the benefit of greater efficiency and transparency. While Google and others benefit from lower-cost public ad exchanges, they join social platforms such as a Facebook and Instagram in building more influential and publically accepted forms of advertising, including video and native.

Bulk ad buying makes all oceans rise, even for the fraud it produces. Don’t misunderstand poor ad quality to be endemic of programmatic, it’s just one of the considerations in your choice of exchange networks.

Part Five. Ad quality in question

Digital advertising has come under attack with a variety of labels and headlines, including click fraud, viewability, pixel stuffing, ad stacking, spoofing and many more. This fraud comes from a variety of human and non-human threats, such as bots trolling the Web and click farms of low wage workers in poverty-stricken countries clicking on ads. Horrible.

Despite this, digital advertising is stronger than ever, reaching new heights in 2017 by outspending television advertising for the first time with $209 billion worldwide or 41% of the market (IPG Mediabrands). In terms of viewability, digital media is not alone, here. Traditional media commonly buys advertising never viewed, magazine ads never read, radio ads never heard, and so on.

In documenting the demise of the 30-second television commercial, a study by metrics firm Aris indicated 84% of viewers commonly fast forward through ads. Yet, advertising on television means your ad dollars are spent even when your viewer runs to the kitchen during the commercials.

Today, click farms, bots and other nefarious schemes are estimated to take in as much as $7 billion in ad revenue. How did we get here? During the great dawn of digital advertising before fraud was ever imagined, popular pay-per-click ads were sold based on their ability to bring traffic to an advertiser’s website.

Competing businesses clicked the ads, triggering a wave of click fraud that had Google scrambling to make refunds and improve tracking. The product evolved to reduce fraud by focusing on a proven sales conversion, where analytics proved purchases and ROI was easily interpreted; a remedy to click fraud.

A major component of this shift is analytics and our ability to track and measure each action. While this tracking ability sets digital apart from traditional forms of advertising, it’s also become the metric by which ad publishers make money. Fooling the analytic means fraudsters can make a lot of money.

Viewability means as much as 50% of digital ads may never be seen (comScore 2016) yet they are paid for by the advertiser. This occurs when a website is loaded into a browser but the ad, which loads a fraction of a second slower, is never seen by the quick scrolling user. Advertisers are buying the ads’ opportunity to be seen by an estimated audience. IAB considers an ad viewable on a desktop computer if 50% of the ads’ pixels are in view for a minimum of 1 second. For video, 50% is required for 2 seconds. For larger display ad units 30% is required for at least 1 second.

Use of programmatic technology has flooded the market with banner ads never seen and perhaps exacerbated the ability for fraud to occur. This is not to say the programmatic and similar artificial intelligence is based on fraud. The fraudsters simply capitalize on the technology to propagate itself. In an effort to filter out the fraudsters, reputable agencies are cultivating white lists of “safe” publishers such as Buzzfeed, Yahoo!, and Weather.com and USA Today.

This provides greater assurances against fraud and enables the agency to market their own safe lists to clients or employ public lists. Ultimately, advertisers want a return on their investment regardless of media type and digital is no different. This is where digital succeeds in measurable ways with its robust target and analytics profiles. At the end of the day, digital advertising boasts greater transparency than any other ad media type.

Implications and opportunities for adaptive marketers

Paradigm shifts in digital advertising have attempted to outpace fraud since the beginning and today the same is true. The invention of native advertising, video and content marketing is helping brands spread their message in a lasting, more meaningful way.

Additionally, advertisers are setting ROI goals, which allow them to better evaluate tier ad spend. Digital remains a good investment and continues to rise in market share among advertisers. Given this paradigm shift, consider the following opportunities for adaptive marketers:

· Is your ROI hitting its target? Measure against ROI: brand awareness lift, education, purchases, phone calls, inquiries, registrations – these are more resistant to fraud

· Use 3rd party tools to capture analytics and demand transparency from agency and publisher

· Target ads above the fold; they have a 68% chance of being seen

· Vertical ads are a safer bet; they are on page longer because of their length

· Realize that quality media will always cost more; be suspicious of “good deals”

· Utilize white listed publishers for programmatic media buys

In summary, Viewability is nothing new to advertising but is the most recent buzzword by which digital is scrutinized. Traditional media suffers too when viewers step away from the television screen or fast-forward through a commercial.

These issues of quality don’t equate to a paradigm shift on their own; however, when combined with enabling technologies such as programmatic, there is an opportunity to degrade the quality of ads, particularly banner ads, in mass numbers as consumers bypass the clutter with slow loading browsers, adblockers, and quick scrolling fingers.

The shift towards higher quality advertising experience means consumers are preferring ads that complement the viewing experience, including video ads, storytelling, content marketing, and native advertising.

Most read in Opinions

Trending articles on Opinions

Top articles on Minutehack

Long Read: Digital Marketing Paradigms At War

Thanks for signing up to Minutehack alerts.

Brilliant editorials heading your way soon.

Okay, Thanks!