Government Borrowing Hits February Record To Pay For Covid-19 Response

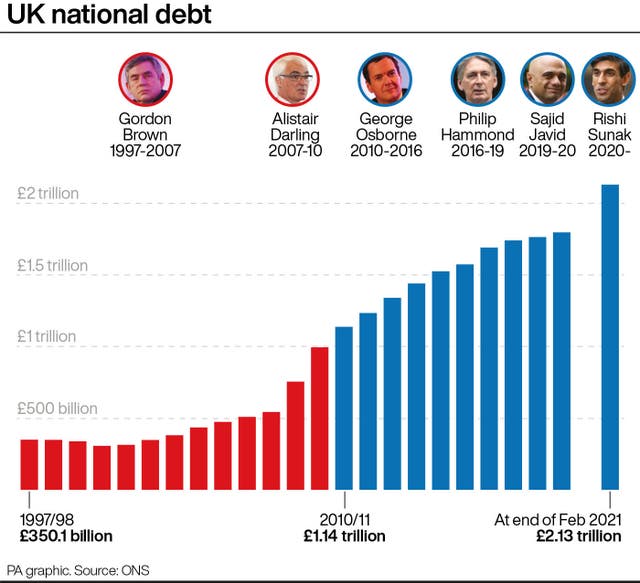

Public sector debt rose above £2 trillion in 2020.

The Government borrowed another £19.1 billion in February as it continues to fund a fight against the Covid-19 pandemic amid the economic toll of lockdown.

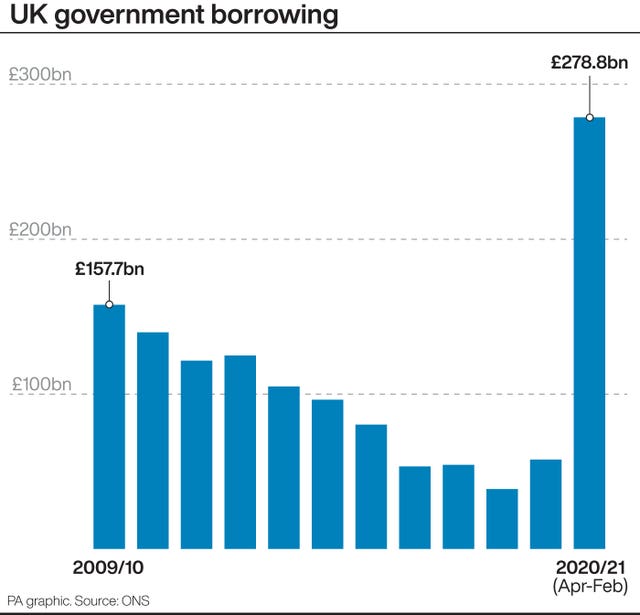

It was the most that the public sector has borrowed during any February since records began in 1993, according to figures from the Office for National Statistics (ONS).

The debt owed by public sector bodies has now risen by £333 billion since April, the first month of full lockdown in the UK.

The total debt is now £2.131 trillion, the ONS said.

Central Government bodies are believed to have spent around £72.6 billion running their day-to-day activities in February.

That is a rise of £14.2 billion compared with February 2020, and includes £3.9 billion on supporting jobs through Covid-19.

Chancellor Rishi Sunak, who has overseen the Treasury’s response to the pandemic, said: “Coronavirus has caused one of the largest economic shocks this country has ever faced, which is why we responded with our £352 billion package of support to protect lives and livelihoods.

“This was the fiscally responsible thing to do and the best way to support the public finances in the medium term.

“But I have always said that we should look to return the public finances to a more sustainable path once the economy has recovered, and at the Budget I set out how we will begin to do just that, providing families and businesses with certainty.”

Mr Sunak pledged early on in the pandemic to provide whatever support businesses needed to help them through the Government-imposed lockdowns.

It has seen the Government back more than £70 billion through three loan schemes, and also pay 80% of salaries to around 10 million workers who were furloughed.

The Government has relied heavily on borrowing to be able to fund this spending as tax receipts have also gone down during the period.

However, Mr Sunak has signalled that tax rises are likely in coming years, already announcing a plan to increase corporation tax from 19% to 25% for large companies by 2023.

Neil Birrell, chief investment officer at Premier Miton, an asset manager, said: “Clearly the Government is more concerned about supporting the economy than anything else at present, but the level of debt needs to be addressed properly in due course.

“Economic growth in itself helps, but so do tax increases.”

Government Borrowing Hits February Record To Pay For Covid-19 Response

Thanks for signing up to Minutehack alerts.

Brilliant editorials heading your way soon.

Okay, Thanks!